Posted By Jeanne Meade | June 01, 2023

The fact that airline operating expenses have recently risen is well published, and led by major factors such as fuel and labor which historically have accounted for the biggest portion of operating expenses. Closely on the heels of fuel and labor are the expenses for maintenance, repair, and overhaul (MRO) of which the cost of parts, repairs, and overhaul have risen disproportionately compared to common economic indices such as Inflation and the Consumer Price Index. I wrote about this likely phenomenon in an article titled “Airline Maintenance Costs Will Go Up” at this link:

https://www.aviationsuppliers.org/AIRLINE-MX-COSTS-WILL-GO-UP

Directly contributing to this atmosphere are many OEMs who continue to wield their monopolistic positions in the manufacturing and MRO marketplaces. This has been carefully heralded in the article above which points further to other supporting articles. High prices, parts shortages, and long lead times; is the industry sitting back idly licking their wounds or are there any countermeasures in play?

Yes, the emerging countermeasures at play include the following:

• Use of PMA alternative parts

• Use of non-OEM repairs such as DER Repairs (Designated Engineering Representative)

• Use of parts from disassembled aircraft, engines, and APUs (Auxiliary Power Units)

• Use of owner produced parts

I have noticed a quiet increase in the use of owner produced parts as operators develop efficient and approved methods to implement this alternative. Similarly, disassembly of aircraft, engines, and APUs is rising in popularity thanks in part to the championing efforts of AFRA, the Aircraft Fleet Recycling Association (see https://afraassociation.org/). On the other hand, it continues to be surprising that PMA and non-OEM repairs such as DER Repairs have not accelerated for these clearly airworthy and approved solutions. By the way, MARPA, the Modification and Replacement Parts Association continues to be a staunch industry advocate for PMA parts (see https://pmaparts.org/).

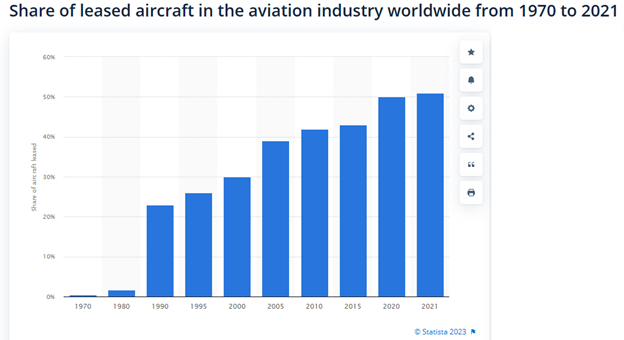

The key question to ask regarding the apparent sluggish growth of PMA and DER Repairs is y tho, since the industry is clearly clamoring for more PMA and DER repairs as reflected in the article ‘MRO Americas: “Unprecedented PMA and DER Demand”' 1. It appears that a key impediment to this comes from the Leasing firms (the Lessors). You’d be forgiven if you were surprised that Lessors can wield this type of influence but consider that approximately 50% of aircraft and 80% of engines are owned by Lessors, and these numbers are growing. Since it is the Lessors that own these assets, they can dictate the terms of the leases to the operators, and this includes restrictions on the use of PMA and DER repairs (non-OEM repairs).

Leasing companies and their spokespersons have come to have an impressive dominant influence on the industry because they literally own the majority of aircraft and engines being flown by airlines. Consider this growth for just aircraft2:

In fact, ‘Even with the COVID-19 pandemic, the aircraft leasing market has found a way to keep growing. The latest report called “Global Aircraft Leasing Market (By Aircraft Type & Region): Insights & Forecast with Potential Impact of COVID-19 (2022-2026)” shows an expected growth at a CAGR of 7.8% during the period spanning from 2022 to 2026, with the global aircraft leasing market forecasted to reach $247.41 billion in 2026’ 3.

All of this begs the question, why are there restrictions on PMA and DER repairs? When asked, the common comeback is that use of PMA and DER repairs lessens the resale or redelivery value of the asset. I researched and asked for the quantitative data supporting this and guess what? Crickets. In the absence of quantitative data and analysis, the idea that these practices will affect resale and redelivery values makes it a perception, not a fact. There, I said it and I meant it.

We must have clearly established in our minds that for operators, the use of PMA and DER Repairs represents opportunities to mitigate rising MRO costs. A recent article ‘The DNA of PMA & non-OEM repairs and cost savings’4 summarizes this very well. So, if this is clearly the case, what can airlines do?

• Choose lessors who will accommodate PMA and non-OEM repairs. Due to the aforementioned financial attractiveness of the Leasing market, there has never been more numbers of lessors available. Globally there are 153 lessors3, and the list is growing. It is my opinion that the number is greater than those 153 cited since I’m not convinced that the list covers smaller sized lessors with limited portfolios. Nonetheless, this represents a considerable choice for lessees; include the availability to use PMA and non-OEM repairs in your decision-making process.

• Renegotiate existing agreements. “Recently carriers such as American Airlines, Delta Airlines, and Copa Airlines have reportedly ditched lessor no-PMA clauses and covenents”4.

It’s my firm belief that with the increased competitiveness among lessors it’s just a matter of time before lessors and lessees come to terms with this. This would be a win-win for both.

Over ‘n out

Roy ‘Royboy’ Resto

www.AimSolutionsConsulting.com

1 https://pmaparts.wpcomstaging.com/2023/04/20/mro-americas-unprecedented-pma-and-der-demand/

2 https://www.statista.com/statistics/1095749/share-leased-aircraft-aviation-industry-worldwide/

3 https://www.aeroclass.org/aircraft-leasing-industry/

4 The DNA of PMA and non-OEM Repairs and cost savings; Aircraft Commerce; Issue No. 145; December 2022 / January 2023; page 23