As promised, here is part II of 2018’s compilation of Facts,

Figures, and Forecasts (F3). The source citations are at the very

end.

Here are the data listings in this order:

- Here’s a listing of the world’s

top defense contractors

- Level of Chinese aviation

expansion revealed by CAAC statistics

- Number of successful ejections

equating to lives saved by Martin Baker Ejection Seats

- Total MRO demand for ATA chapter

25 is $3.7 Billion for 2018 and 2019

- Boeing: 128,500 pilots to be

needed in China by 2037

- IATA: First time ever passenger

numbers exceed 4 billion

- ICAO releases 2018 safety report

- Boeing forecasts air cargo traffic

to double in 20 years

- The future of low cost

- Lasers being pointed at aircraft

- Air transport supports 65.5

million jobs and $2.7 trillion in economic activity

- Airbus: China will need more than

7,400 new aircraft in the next 20 years

- India: new airport and travel

activity

- General Aviation Aircraft

manufacturing outlook positive for 2019

- Airbus: Fleet in Russia and CIS to

double by 2037

- Facts about the FAA and Air

Traffic Control

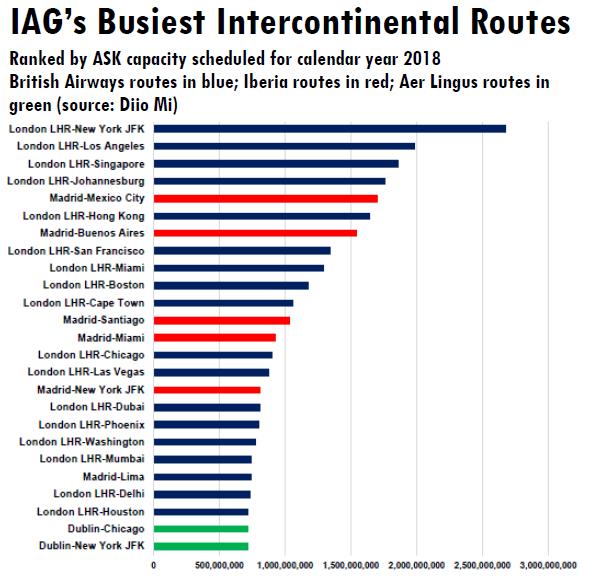

- IAG’s Busiest Intercontinental

Routes

- Global survey reveals anticipated

significant growth in aviation jobs

- And you though your travel budget

was high?

- Russian Military Aircraft Fleet

- New Entrants for Electric

Propulsion

- How Large is the Global Aerospace

Industry?

- Africa becoming new opportunity

continent for emerging airlines

- NATO Aircraft Distribution

Here’s a

listing of the world’s top defense contractors1:

| Rank |

Company |

Country |

2017 Defense

Revenue* (in millions) |

Revenue From

Defense |

| 1 |

Lockheed Martin 1 |

U.S. |

$47,985.00 |

94% |

| 2 |

Raytheon Company 1 |

U.S. |

$23,573.64 |

93% |

| 3 |

BAE Systems |

U.K. |

$22,380.04 |

88% |

| 4 |

Northrop Grumman 2 |

U.S. |

$21,700.00 |

84% |

| 5 |

Boeing 3 |

U.S. |

$20,561.00 |

22% |

| 6 |

General Dynamics 4 |

U.S. |

$19,587.00 |

63% |

| 7 |

Airbus |

Netherlands/France |

$11,185.91 |

15% |

| 8 |

Almaz-Antey 5 |

Russia |

$9,125.02 |

100% |

| 9 |

Thales |

France |

$8,926.13 |

50% |

| 10 |

Leonardo |

Italy |

$8,856.48 |

68% |

| 11 |

United Technologies |

U.S. |

$7,826.00 |

13% |

| 12 |

L3 Technologies |

U.S. |

$7,749.00 |

81% |

| 13 |

Huntington Ingalls Industries |

U.S. |

$7,030.00 |

95% |

| 14 |

United Aircraft Corp. 7 |

Russia |

$6,197.25 |

80% |

| 15 |

Leidos |

U.S. |

$5,218.00 |

51% |

| 16 |

Rolls-Royce |

U.K. |

$4,625.73 |

16% |

| 17 |

Booz Allen Hamilton |

U.S. |

$4,320.00 |

70% |

| 18 |

Naval Group |

France |

$4,178.33 |

100% |

| 19 |

Harris Corporation |

U.S. |

$4,158.00 |

70% |

| 20 |

Textron Inc. |

U.S. |

$4,117.42 |

29% |

Level of

Chinese aviation expansion revealed by CAAC statistics2

- According to the Civil Aviation

Administration of China (CAAC), 93 new general aviation airports were licensed

in the first half of 2018, more than doubling the number of general aviation

airports in the country. China now has 231 civil airports in a total of 404

airports which support the take-off and landing of general aviation aircraft.

- 118 new general aviation aircraft

were registered with the CAAC in the first half of the year, bringing the

country’s total to 2,415 with a 9.5-percent year-on-year increase.

- Currently, China has direct air

routes with 45 countries alongside the Belt and Road, operating roughly 5,100

flights per week. CAAC has also signed documents with the Czech Republic,

Kazakhstan, New Zealand and Australia to secure civil aviation cooperation.

Number of

successful ejections equating to lives saved by Martin Baker Ejection Seats3

Total MRO

demand for ATA chapter 25 is $3.7 Billion for 2018 and 20194

- Over the next two years,

commercial, regional and business aircraft will go through $3,700,958,983 worth

of total MRO demand.

- ATA chapter 25 is comprised of :

Flight Compartment, Passenger Compartment, Buffet/Galley, Lavatories, Cargo

Compartments, Emergency, Accessory Compartments, Power Drive Units, Coffee

Makers, Water Heaters, Boilers, Etc.

Boeing:

128,500 pilots to be needed in China by 20375

- Boeing reports that the Asia

Pacific region will have the greatest global demand for new civil aviation

personnel over the next 20 years. The region is projected to account for 33

percent of the global need for pilots, 34 percent for technicians and 36

percent for cabin crew.

- Forty percent of all new passenger

airplane deliveries in the next 20 years will be delivered to airlines in the

Asia Pacific, also making the region leading in personnel demand, according to

2018 Boeing Pilot & Technician Outlook - an industry forecast, tied to

projections for new airplane deliveries.

- New commercial technician demand

decreased five percent to 242,000. This is due to advancements in product

development on the 737 MAX, which have resulted in increased maintenance

efficiencies. Overall, maintenance hours required over the life of the airplane

will be reduced.

- New commercial cabin crew demand

increased three percent to 317,000 due to anticipated fleet mix, cabin

configuration and regulatory requirements.

- Including the demand in the

helicopter and business aviation markets, 261,000 pilots, 257,000 technicians

and 321,000 cabin crew will be needed in the region.

- Leading the region in projected

demand for new pilots, technicians and cabin crew:

- China: 128,500 pilots; 126,750

technicians; 147,250 cabin crew

- Southeast Asia: 48,500 pilots;

54,000 technicians; 76,250 cabin crew

- South Asia: 42,750 pilots; 35,000

technicians; 43,250 cabin crew

IATA: First time ever passenger

numbers exceed 4 billion6

Worldwide annual air

passenger numbers exceeded four billion for the first time in 2017, the

International Air Transport Association (IATA) announced on September 6, 2018.

In its industry performance statistics for 2017, the association also observes

that airlines connected a record number of cities worldwide, providing regular

services to over 20,000 city pairs in 2017, more than double the level of 1995.

The unprecedented

passenger numbers growth is supported by a broad-based improvement in global

economic conditions and lower average airfares, according to IATA. “In 2000,

the average citizen flew just once every 43 months. In 2017, the figure was

once every 22 months,” said Alexandre de Juniac, IATA’s Director General and

CEO.

The association also

provides the following data of the 2017 airline industry performance:

Passenger

- System-wide,

airlines carried 4.1 billion passengers on scheduled services, an increase of

7.3% over 2016, representing an additional 280 million trips by air.

- Airlines

in the Asia-Pacific region once again carried the largest number of passengers.

The regional rankings (based on total passengers carried on scheduled services

by airlines registered in that region) are:

1. Asia-Pacific 36.3% market share (1.5 billion passengers, an increase of

10.6% compared to the region’s passengers in 2016)

2. Europe 26.3% market share (1.1 billion passengers, up 8.2% over

2016)

3. North America 23% market share (941.8 million, up 3.2% over 2016)

4. Latin America 7% market share (286.1 million, up 4.1% over 2016)

5. Middle East 5.3% market share (216.1 million, an increase of 4.6% over

2016)

6. Africa 2.2% market share (88.5 million, up 6.6% over 2016).

- The

top five airlines ranked by total scheduled passenger kilometers flown, were:

1. American

Airlines (324 million)

2. Delta Air Lines (316.3 million)

3. United Airlines (311 million)

4. Emirates Airline (289 million)

5. Southwest Airlines (207.7 million)

- The

top five international/regional passenger airport-pairs** were all within the

Asia-Pacific region, again this year:

1. Hong Kong-Taipei Taoyuan

(5.4 million, up 1.8% from 2016)

2. Jakarta Soekarno-Hatta-Singapore (3.3 million, up 0.8% from 2016)

3. Bangkok Suvarnabhumi-Hong Kong (3.1 million, increase of 3.5% from

2016)

4. Kuala Lumpur–Singapore (2.8 million, down. 0.3% from 2016)

5. Hong Kong-Seoul Incheon (2.7 million, down 2.2% from 2016)

- The

top five domestic passenger airport-pairs** were also all in the Asia-Pacific

region:

1. Jeju-Seoul Gimpo (13.5

million, up 14.8% over 2016)

2. Melbourne Tullamarine-Sydney (7.8 million, up 0.4% from 2016)

3. Fukuoka-Tokyo Haneda (7.6 million, an increase of 6.1% from

2016)

4. Sapporo-Tokyo Haneda (7.4 million, up 4.6% from 2016)

5. Beijing Capital-Shanghai Hongqiao (6.4 million, up 1.9% from 2016)

- One

of the interesting recent additions to the WATS report is the ranking of

passenger traffic by nationality, for international and domestic travel.

(Nationality refers to the passenger’s citizenship as opposed to the country of

residence.)

1. United States of America

(632 million, representing 18.6% of all passengers)

2. People’s Republic of China (555 million or 16.3% of all

passengers)

3. India (161.5 million or 4.7% of all passengers)

4. United Kingdom (147 million or 4.3% of all passengers)

5. Germany (114.4 million or 3.4% of all passengers)

Cargo

- Globally,

cargo markets showed a 9.9% expansion in freight and mail tonne kilometers

(FTKs). This outstripped a capacity increase of 5.3% increasing freight load

factor by 2.1%.

- The

top five airlines ranked by scheduled freight tonne kilometers flown were:

1. Federal Express (16.9 billion)

2. Emirates (12.7 billion)

3. United Parcel Service (11.9 billion)

4. Qatar Airways (11 billion)

5. Cathay Pacific Airways (10.8 billion)

Airline

Alliances

- Star Alliance

maintained its position as the largest airline alliance in 2017 with 22%

of total scheduled traffic (in RPKs), followed by SkyTeam (19%) and oneworld

(16%).

ICAO releases 2018 safety report7

- The

International Civil Aviation Organization (ICAO) observes a general trend of

lower number of fatal accidents and fatalities over the past ten years,

according to the findings in its 2018 edition of its Safety Report, released

this week.

The report summarizes the organizations safety

initiatives in 2017 and provides safety performance indicators in 2013–2017.

- In 2017,

there were 4.1 billion passengers travelling by air worldwide on scheduled

commercial services, the organization summarized in a statement released on

September 5, 2018. ICAO accounts 5 fatal accidents and 50 passenger deaths in

2017, putting the commercial aviation safety rate at 12.2 fatalities per

billion passengers and confirming its previous proclaim that 2017 was the

safest year on the record in aviation history.

ICAO claims it remains “particularly focused on its

safety priorities”, including Runway Safety, Controlled Flight into Terrain

(CFIT), Loss of Control Inflight (LOCI), and new safety initiatives. In 2018

report, it notes that global average of effective implementation of ICAO

Standards and Recommended Practices increased from 64.7 % in 2016 to 65.5% in

2017.69.19 % of 192 member states have

achieved the 60 % target, set by the Global Aviation Safety Plan (GASP)

2017–2019 edition.

Boeing

forecasts air cargo traffic to double in 20 years8

- Boeing projects air cargo

operators will need more than 2,600 freighters over the next two decades to

keep up with increasing global freight traffic, which is expected to double

with 4.2 percent growth annually.

- The 980 new medium and large freighters

and 1,670 converted freighters will go toward replacing older airplanes and

growing the global fleet to meet demand, according to the new World Air Cargo

Forecast, released by Boeing today at The International Air Cargo Association's

Air Cargo Forum and Exhibition.

- Some of the factors driving the

growth in air cargo include a growing express market in China and the global

rise of e-commerce, which is forecast to increase 20 percent annually to nearly

$5 trillion in 2021 according to Boeing's analysis.

To meet growing market needs, Boeing also forecasts:

- The world freighter fleet will

expand by more than 70 percent, from the current total of 1,870 to 3,260

airplanes.

- Demand for regional express

services in fast-developing economies will boost the standard-body share of the

freighter fleet from 37 percent today to 39 percent.

- 1,170 standard body and 500 medium

wide-body passenger airplanes will be converted into freighters over the next

two decades.

The future

of low cost9 (Article excerpts regarding Low Cost Carriers, LLC’s)

- Today, half a century later, low

cost has become the preferred means of travel for a third of the world's

passengers. It is estimated that in 2027 - that is, within ten years - half of

the nearly 7 billion flights globally will be of this type.

- The consultant OAG estimates that

this year more than 50 percent of travelers from 10 European countries are

already choosing low-cost airlines. Macedonia tops this list; however, the

country that offers most low-cost seats is Spain, with 82.2 million last year.

Meanwhile, Irish airline Ryanair is a leading low cost carrier, but due its

labor problems this year, it can be overtaken by Easyjet. The low cost model

has provided the means of travel to many people, who were previously unable to

do it.

- Another rising phenomenon is the

so-called low-cost, long-range (low-cost long-haul) – a bet, already taken by

Norwegian. 20% of its fleet is currently devoted to such flights, and the

airline is already expanding, by adding subsidiary in Argentina or opening new

transoceanic routes like the one planned between London and Rio de Janeiro.

Lasers being pointed at aircraft10

- Laser strikes on aircraft and

helicopters have risen over the years and laser pointers are increasing in

power and decreasing in price. Lasers can distract and even harm pilots during

critical phases of flight and can cause temporary visual impairment. Over 6750

laser incidents were recorded in the USA in 2017 according to the Federal

Aviation Administration. In 2016 there were over 1750 laser incidents reported

to the UK Civil Aviation Authority and Transport Canada Civil Aviation.

Air

transport supports 65.5 million jobs and $2.7 trillion in economic activity11

- The global air transport sector

supports 65.5 million jobs and $2.7 trillion in global economic activity,

according to new research released today by the Air Transport Action Group

(ATAG).

- "There are over 10 million

women and men working within the industry to make sure 120,000 flights and 12

million passengers a day are guided safely through their journeys. The wider

supply chain, flow-on impacts and jobs in tourism made possible by air transport

show that at least 65.5 million jobs and 3.6% of global economic activity are

supported by our industry."

Key facts outlined in Aviation: Benefits Beyond Borders,

include:

- -Air transport supports 65.5

million jobs and $2.7 trillion in global economic activity.

- -Over 10 million people work

directly for the industry itself.

- -Air travel carries 35% of world

trade by value ($6.0 trillion worth in 2017), but less than 1% by volume (62

million tonnes in 2017).

- -Airfares today are around 90%

lower than the same journey would have cost in 1950 – this has enabled access

to air travel by greater sections of the population.

- -If aviation was a country, it

would have the 20th largest economy in the world – around the same size as

Switzerland or Argentina.

- -Aviation jobs are, on average,

4.4 times more productive than other jobs in the economy.

- -Scope of the industry: 1,303

airlines fly 31,717 aircraft on 45,091 routes between 3,759 airports in

airspace managed by 170 air navigation service providers.

- -57% of world tourists travel to

their destinations by air.

Airbus:

China will need more than 7,400 new aircraft in the next 20 years12

- China will need over 7,400 new

passenger aircraft and freighters from 2018 to 2037, with a total market value

of US $1,060 billion, according to Airbus’ latest China Market Forecast. It

represents more than 19% of the world total demand for over 37,400 new aircraft

in the next 20 years.

India: new

airport and travel activity13

- Kishangarh is one of 34 airports

opened in the past 18 months in India, whose aviation sector has exploded in

the wake of massive economic growth. In September, the civil aviation minister

said that $60 billion has been budgeted for 100 more in the next 10 to 15

years.

- By 2024, the IATA estimates, India

will rank behind only China and the United States in terms of air traffic to,

from and within the country.

General

Aviation Aircraft manufacturing outlook positive for 201914

The General Aviation Manufacturers Association expressed

optimism about the industry’s prospects for 2019.

- The piston rotorcraft delivery

number of 220 units headlined the year-to-date figures, and marked a

15.8-percent increase from 2017’s third-quarter figure of 190 units delivered.

Turbine rotorcraft shipments accelerated by 8.3 percent, from 471 units

delivered to 510.

- The 784 piston airplanes

deliveries marked an improvement over the comparable 2017 period’s tally of

724, for a gain of 8.3 percent. Turboprop airplane shipments came in at 395 for

a 5.6-percent increase over the 374 deliveries of the first three quarters of

2017.

- Business jet shipments increased

from 433 to 446, or 3 percent, not far off last year’s totals through three

quarters.

- Looking at selected manufacturers

and results reported by GAMA, Cirrus Aircraft shipped 106 airplanes in the

third quarter consisting of 90 singles and 16 SF50 Vision jets. Cirrus’s total

shipments for the year to date added up to 303 aircraft.

- Diamond Aircraft had its best

quarter of the year in terms of shipments with 14 twin-engine DA–42 and 15

DA–62 models accounting for 76 percent of the quarter’s total.

- Brazilian manufacturer Embraer

shipped 15 Phenom 300 10-seat jets during the quarter; the aircraft has been

noted as an emerging sector leader and has accounted for 24 of the company’s 55

overall aircraft shipments year to date, or 44 percent.

- Swiss manufacturer Pilatus shipped

27 aircraft in the quarter, consisting of 20 PC–12 single-engine turboprops,

six of its new PC–24 jets, and one STOL workhorse PC–6 Porter. The company has

shipped 62 airplanes to date.

- Among the 65 singles, twins, and

M-class variants shipped by Piper in the third quarter were 34 PA–28–181 Archer

III airplanes, as Piper pursued its declared strategy of focusing on the flight

training marketplace. The activity brought the total of aircraft shipped so far

this year to 152.

- The year’s trend continued in

Textron Aviation’s Cessna unit, where shipments of Skyhawk SP (30) piston

singles and Grand Caravan EX (21) turboprops led the way. Thirteen Citation

Latitude jets shipped in the quarter, with the three models combining to

account for 64 percent of Cessna’s 110 total third-quarter shipments.

- Bell 505 Jet Rangers, the Leonardo

AW139, and Robinson Helicopters’ R44 piston and R66 turbine models showed

strength among rotorcraft, with the Robinson piston helicopter models and

variants representing the majority of the increased rotorcraft deliveries, GAMA

noted for the period.

Airbus: Fleet

in Russia and CIS to double by 203715

According to Airbus’ Global Market Forecast, unveiled at the

Wings of the Future conference in Moscow:

- Russia and CIS’s airlines will

need some 1220 new aircraft valued at US$175 billion in the upcoming 20 years

(2018-2037).

- This means that the passenger fleet

in the region will almost double from 857 aircraft in service today to over

1700 by 2037.

- Over the next 20 years, passenger

traffic in Russia and CIS region will grow at the average rate of 4.1% annually

with Russia being the major contributor to this growth.

- By 2037 the propensity for air

travel in Russia will more than double.

Facts about

the FAA and Air Traffic Control16

- At

any given moment there are more than 5,000 aircraft traversing the U.S. skies.

- The

FAA is a year-round 24/7 operation, responsible for 5.3 million square miles of

U.S. domestic airspace and 24 million square miles of U.S. airspace over the

oceans.

- There

are 43,290 average daily flights in and out of the U.S.

- More

than 14,000 air traffic controllers manage traffic from many of the FAA’s 700

facilities.

- Fifty-five

hundred airway transportation system specialists maintain more than 70,000

pieces of equipment.

- Aviation

contributes $1.6 trillion annually to the U.S. economy and constitutes 5.1

percent of the gross domestic product.

- Aviation

generates 10 million jobs in the U.S. annually.

Global

survey reveals anticipated significant growth in aviation jobs18

IATA has revealed the results of a global survey of over 100

leading industry HR professionals at airlines, airports and ground service

providers, carried out by Circle Research to learn more about how HR decision-makers

were managing the retention, training and recruiting of skilled professionals

to fill the anticipated job gaps.

In brief, the results of the report showed that:

- More than 73% of respondents

expect the major areas of job growth to be in ground operations, customer

service and cabin crew.

- 48% reported that finding new

talent is a challenge, through lack of availability of candidates with the

right skill levels and qualifications, plus salary demands of new applicants.

- In addition to the salary and benefits

package of each employee, the HR professionals identified career progression

opportunities (49%) and development and training (33%) as high priorities in

job satisfaction and retention.

- Only 28% of respondents reported

that current training is effective, with many organizations seeking to

complement their in-house training with external partners to improve the

effectiveness of the training.

- Safety and customer service skills

are priorities for hiring managers across the industry. While technology is

indeed changing the customer service role, it is not replacing it.

- Approximately 75% of respondents

expected an increase in customer service, ground operations and cabin crew jobs

over the next two years.

- That is higher than the 65% of

respondents that expect growth in security jobs and 63% that expect growth in

regulatory positions.

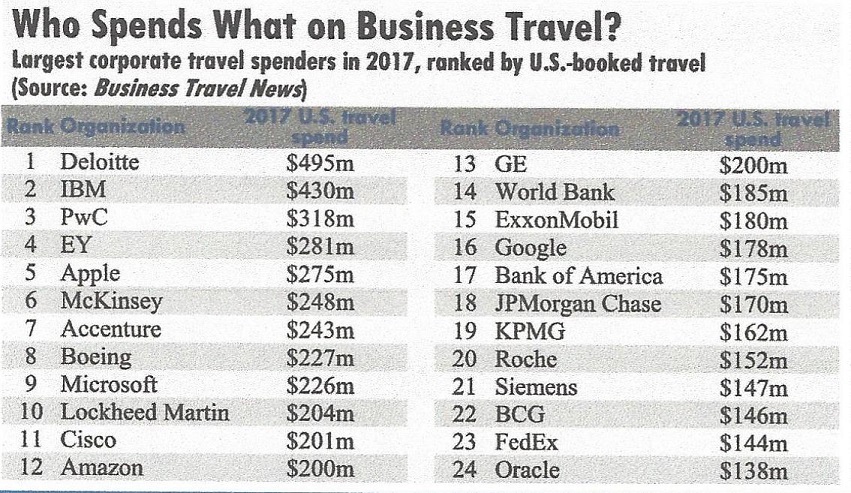

And you

though your travel budget was high?Source noted

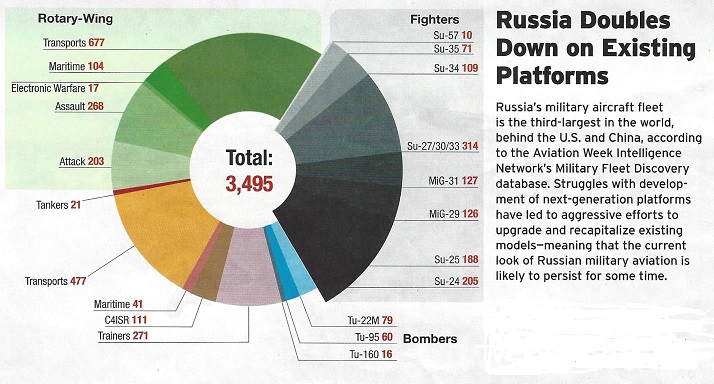

Russian Military Aircraft Fleet19

New

Entrants for Electric Propulsion20

- Almost 100 electrically propelled

aircraft are in development worldwide.

- 60% of these are being conducted by

startups, the rest are traditional aerospace incumbents.

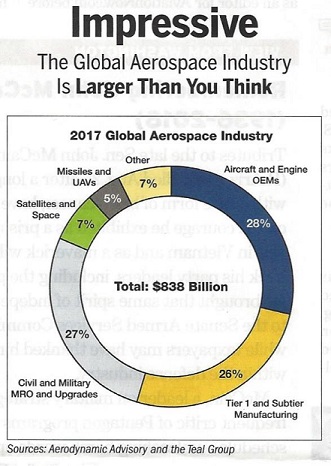

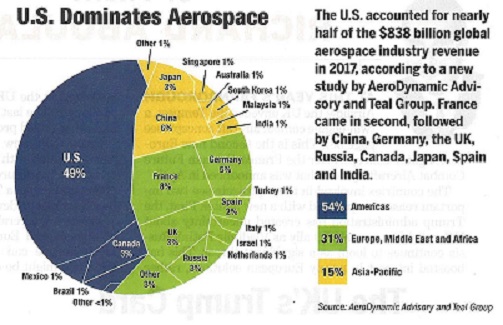

How Large is the Global Aerospace Industry? 21

Africa becoming new opportunity continent for emerging

airlines22

- According to the data from IATA,

Africa is home to 16% of the world’s population but it accounts for only 2.20%

of the global air service market.

- According to data available from IATA

the Revenue Passengers Kilometer (RPK) grew by 6.3% and the Freight

Tonne-Kilometres (FTK) grew by 24.8%, the highest of any continent.

- Yet, despite these good numbers put up

by Africa indicating strong growth, its traffic share of total passengers

remains the lowest of any continent at only 2.20% of the world share. The

passenger traffic share trend is improving however, compared to 2016 African

airlines saw a 7.5% traffic rise in 2017 but with existing infrastructure capacity

rose at less than half the rate of demand.

- By 2026 passenger numbers are expected

to increase from 100 million to more than 300 million. This explosive growth

corresponds to 5.9% year-on-year growth.

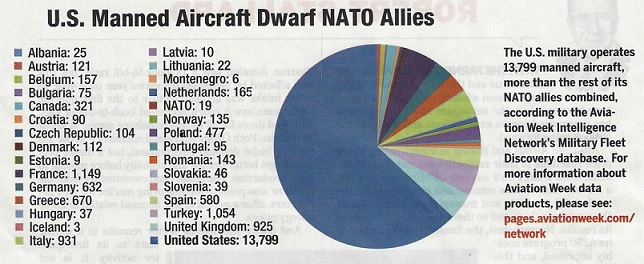

NATO Aircraft Distribution23

Roy ‘Royboy’

Resto

President/FAA-DAR

www.AimSolutionsConsulting.com

1

http://people.defensenews.com/top-100/

2 Level

of Chinese aviation expansion revealed by CAAC statistics; Avitrader; Daily

Aviation News Alert; Wednesday, August 15th, 2018

3 https://www.linkedin.com/feed/update/activity:6437...

4 https://www.skylinkintl.com/blog/the-two-year-mro-...

5 https://www.aerotime.aero/aerotime.team/21705-boei...

6 https://www.aerotime.aero/aerotime.team/21775-iata...

7 https://www.aerotime.aero/aerotime.team/21784-icao...

8 https://www.aerotime.aero/aerotime.team/21986-boei...

9 https://www.aerotime.aero/aerotime.team/21998-the-...

10 https://www.avitrader.com/2018/10/23/satair-and-me...

11 http://speednews.com/Article/115981?NL=SPD-01&Issu...

12 https://www.avitrader.com/2018/11/08/china-will-ne...

13 https://www.washingtonpost.com/world/asia_pacific/...

14 https://www.aopa.org/news-and-media/all-news/2018/...

15https://www.avitrader.com/2018/11/21/fleet-in-russ...

16

https://www.faa.gov/news/fact_sheets/news_story.c...

17 Airline

Weekly, Oct 22, 2018, Issue 692, Page 5

18

https://www.avitrader.com/2018/08/20/global-surve...

19

Aviation Week & Space Technology; September 17-30, 2018, page 10

20

Aviation Week & Space Technology; September 3-16, 2018, page 28

21 Aviation Week

& Space Technology; September 3-16, 2018, page 12

Aviation Week & Space Technology;

July 30-August 19, 2018, page 11

22https://www.aerotime.aero/aerotime.team/21642-afri...

23 Aviation Week & Space Technology; August 20-September

2, 2018, page 11